When it comes to protecting your vehicle, knowing the right coverage and rates can save you both money and stress. You might be wondering how much comprehensive vehicle cover really costs and what factors influence those rates.

Whether you’re shopping in Austin, Texas, or anywhere else, understanding comprehensive cover rates helps you make smarter decisions for your car insurance. You’ll discover clear explanations and practical tips to find the best coverage at the right price—so you can feel confident that your vehicle is fully protected without paying more than you need to.

Keep reading to uncover what drives your rates and how to get the most value from your insurance.

Comprehensive Coverage Basics

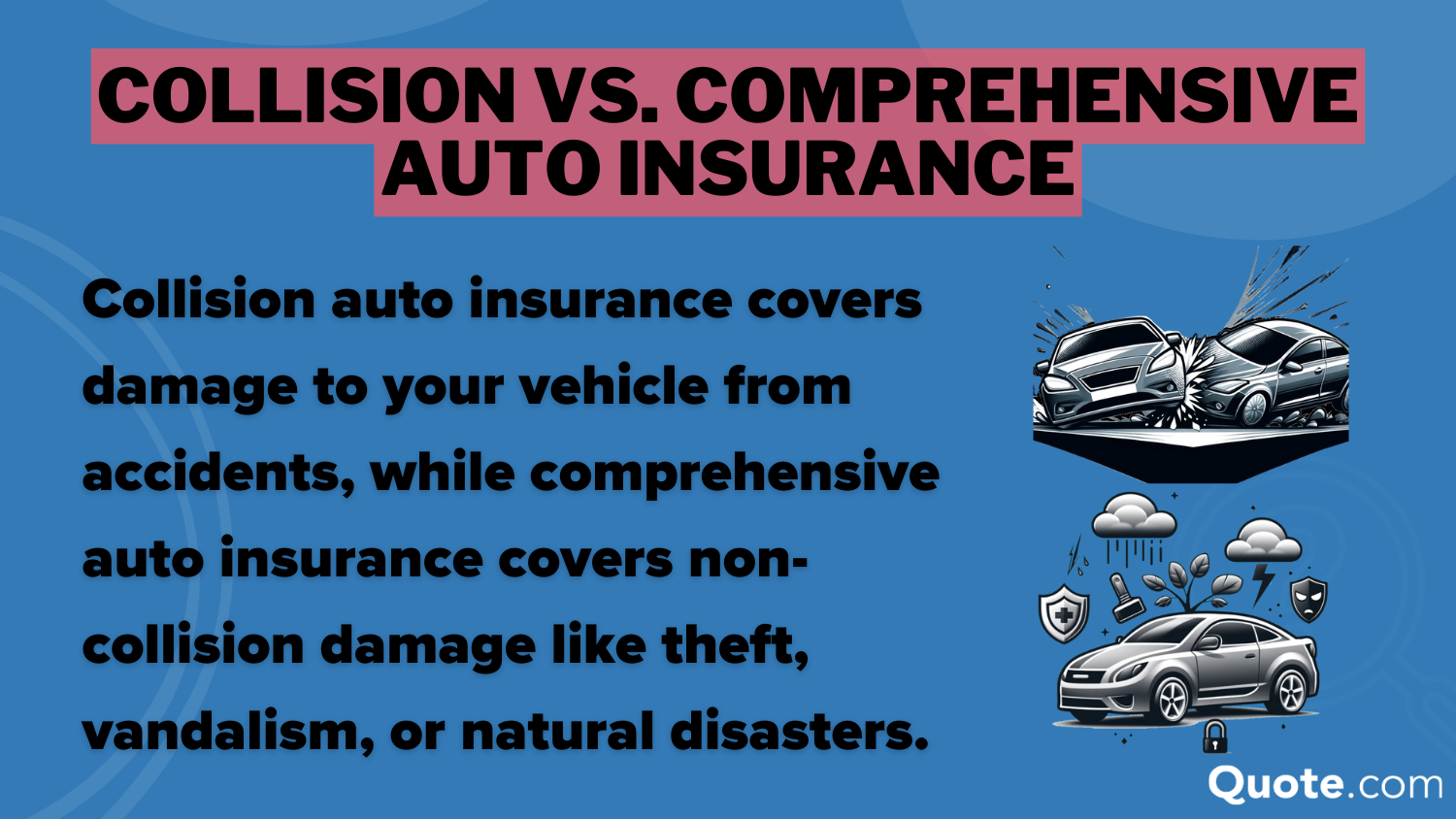

Comprehensive coverage protects your vehicle from damage not caused by a collision. It covers things like theft, vandalism, fire, and weather damage. This coverage also pays for broken glass or animal hits.

Unlike collision insurance, comprehensive does not cover crashes. Collision insurance only pays when you hit another car or object. Comprehensive covers more risks outside driving accidents.

People who park their car on the street or in risky areas benefit most. It helps if you live where natural disasters happen often. Also good for those who want extra protection beyond basic insurance.

Factors Affecting Rates

Vehicle type and model affect insurance costs significantly. Larger or luxury cars usually cost more to insure. Small cars or older models often have lower rates. Some cars are safer, so rates vary by model.

Driver age and history also matter. Younger drivers pay more because they have less experience. Drivers with accidents or tickets face higher premiums. Safe driving history helps lower rates.

Location impact can change rates too. Areas with more theft or accidents tend to have higher premiums. Urban places often cost more than rural areas. Local laws and weather also influence costs.

Coverage limits set how much the insurer pays. Higher limits mean higher premiums. Lower limits save money but increase risk. Choosing the right balance is important for good protection.

Average Costs Breakdown

Vehicle type greatly affects comprehensive coverage costs. SUVs often cost more to insure than sedans or hatchbacks. Luxury cars have the highest premiums due to expensive repairs.

| Vehicle Type | Average Annual Premium |

|---|---|

| SUV | $1,200 |

| Hatchback | $900 |

| Sedan | $850 |

| Luxury | $1,800 |

Monthly premiums are usually higher than annual rates divided by 12. Paying yearly can save up to 10% on total costs.

Rates vary by region. Urban areas tend to have higher premiums due to theft and accident risks. Rural areas often see lower costs.

Higher deductibles lower your premium but increase out-of-pocket costs during claims. Choosing the right deductible balances risk and savings.

Ways To Lower Your Premium

Safe driving discounts reward drivers with clean records. They can lower premiums by 10% or more. Staying accident-free shows responsibility and helps insurers trust you.

Bundling insurance policies means combining auto and home insurance. This often saves money on both policies. Many companies offer a discount for bundling.

Choosing higher deductibles reduces your monthly payment. You agree to pay more out of pocket if a claim happens. This lowers the insurer’s risk and your premium.

Usage-based insurance tracks driving habits through a device or app. Safe, low-mileage drivers get lower rates. It rewards careful and less frequent driving.

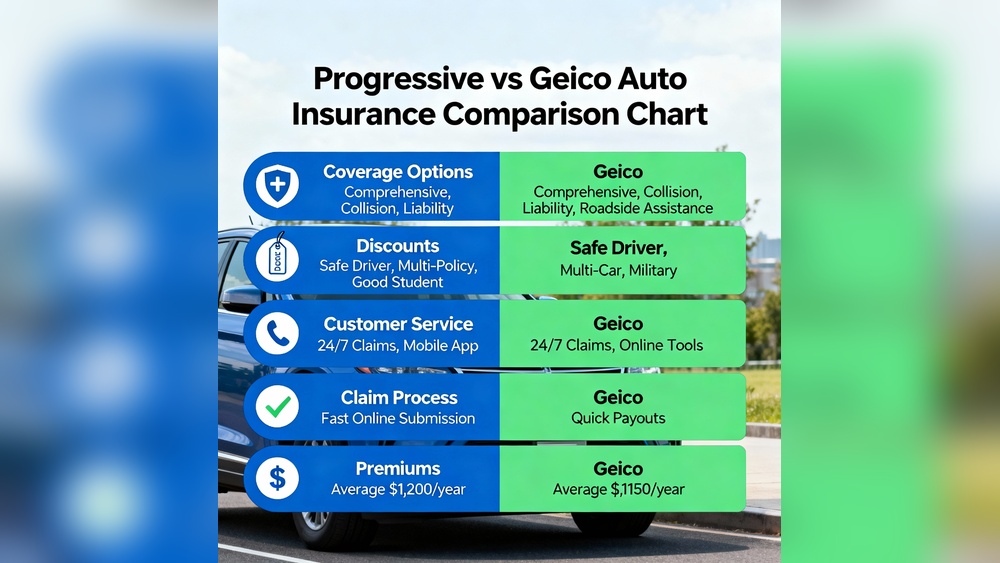

Comparing Insurance Providers

Austin, Texas offers many top insurance companies. Some of the most popular are GEICO, Allstate, Progressive, and State Farm. They provide good rates and coverage options. Most companies have easy online quote tools. These tools help customers get quick price estimates. They often ask simple questions about your car and driving history.

Customer service is very important. Many companies have phone support, chat, and email help. Reading online reviews shows how happy customers are. Look for companies with high ratings and fast response times.

Policy flexibility means you can choose different coverages. Some let you add extras like rental car coverage or roadside assistance. This helps you get the right plan for your needs. You can also change your policy as your life changes.

Using Rate Calculators

Online rate calculators help estimate vehicle insurance costs fast. Enter basic details like car make, model, year, and your location. Some ask for your driving history and coverage preferences. This info helps generate a personalized quote.

Results show estimated monthly or yearly premiums. Compare different coverage levels to find what fits your needs. Pay attention to deductibles and coverage limits. These affect the final price and protection.

| Calculator | Features | Best For |

|---|---|---|

| Allstate | Simple interface, detailed coverage options | Users wanting clear cost breakdowns |

| GEICO | Personalized estimates, coverage advice | People needing tailored protection |

| The Zebra | Compare multiple insurers quickly | Shoppers seeking best deals fast |

Full Coverage Vs Comprehensive

Full coverage combines liability, collision, and comprehensive insurance. It protects against damage from accidents, theft, and natural events. Comprehensive coverage only covers damage not caused by a crash, like theft or weather damage. Full coverage is broader but costs more.

| Coverage Type | What It Covers | Typical Cost |

|---|---|---|

| Full Coverage | Liability + Collision + Comprehensive | Higher premiums |

| Comprehensive | Theft, Fire, Weather, Vandalism | Lower premiums |

Choosing depends on your car’s value, budget, and risk tolerance. Full coverage suits newer or expensive cars. Comprehensive may fit older vehicles or if collision risk is low.

Common Myths About Comprehensive Insurance

Comprehensive insurance does not always raise your rates significantly. Many factors influence the cost, such as your vehicle, location, and driving record. Sometimes, adding comprehensive coverage might increase your premium by a small amount, but it protects you from many risks like theft, weather damage, and vandalism.

Paying for comprehensive coverage can be worth the cost if you want peace of mind. It covers damages that collision insurance does not, saving you money in case of unexpected events. Without it, you might pay a lot out of pocket for repairs or replacement.

Several myths exist about what comprehensive insurance covers. It does not cover damages from collisions or regular wear and tear. Instead, it covers things like fire, natural disasters, and animal damage. Understanding these points helps avoid confusion and choose the right coverage for you.

Frequently Asked Questions

Does Comprehensive Coverage Raise Rates?

Comprehensive coverage can raise rates because it protects against non-collision damages. Rates depend on vehicle type, location, and claims history.

How Much Should Full Coverage Cost On A Car?

Full coverage car insurance typically costs $100 to $200 monthly. Rates vary by location, vehicle type, driver history, and coverage limits.

Is It Better To Have A $500 Deductible Or $1000?

A $500 deductible costs more monthly but lowers out-of-pocket during claims. A $1000 deductible has lower premiums but higher claim expenses. Choose based on your budget and risk comfort.

How Much Is A Comprehensive Cover?

Comprehensive car insurance costs vary by vehicle type, location, and driver profile. On average, expect $100 to $200 monthly.

Conclusion

Choosing the right comprehensive vehicle cover helps protect your car and your wallet. Rates vary based on your car type, location, and driving habits. Comparing quotes ensures you find the best price for your needs. Understanding coverage details prevents surprises during claims.

Stay informed and review your policy yearly to keep up with changes. Protect your vehicle wisely with a plan that fits your budget.

Read More

- Commercial Umbrella Coverage Cost: What You Need to Know Today

- Property Coverage Quote Estimate: Get Fast, Accurate Savings Today

- Fleet Coverage Insurance Quote: Get the Best Rates Today!

- Best Protection Plan Quotes: Unlock Top Savings Today!

- Multi Policy Insurance Savings: Maximize Discounts & Protect More

- Secure Insurance Coverage Review: Maximize Protection Today

- Collision Coverage Quote Online: Get Instant, Affordable Rates Today

- High Limit Coverage Options: Maximize Protection with Top Plans

- Coverage Vault Policy Comparison: Ultimate Guide to Smart Choices

- Auto Coverage Limits Guide: Maximize Your Protection Today